On the 18th of the month, TrendForce released the latest prices of the photovoltaic industry chain.

Silicon Material Prices

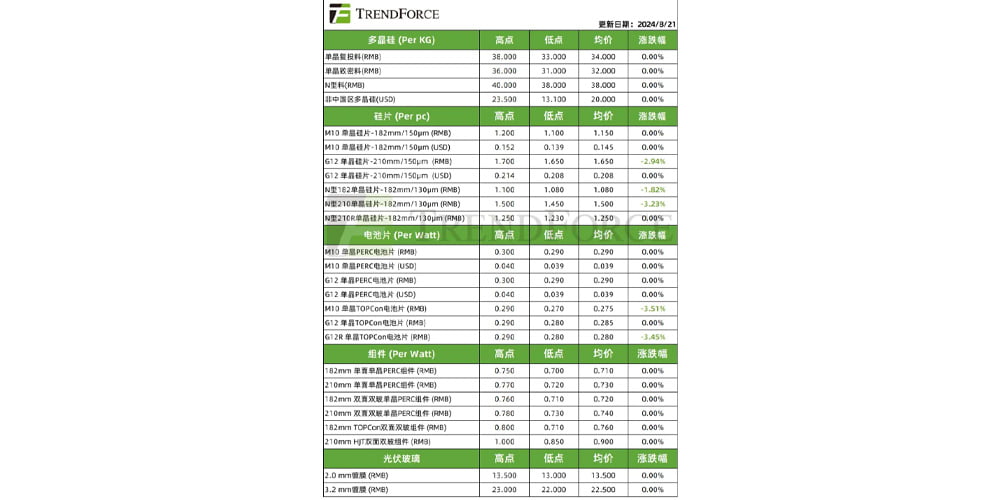

Extrusion Effect Of Silicon Materials This week’s silicon material prices: the mainstream transaction price for monocrystalline recycled materials is 34 yuan / KG, and the mainstream transaction price for monocrystalline dense materials is 32 yuan / KG; N-type materials are priced at 38 yuan / KG.

Trading Situation

This week, small-scale transactions dominated the silicon material market. With tight cash flow at all levels and downstream lacking large-scale transaction intentions, the strategy of buying as needed continues.

Supply Dynamics

Top manufacturers continue to advance production reduction plans, with the scale of production cuts potentially expanding. Despite the extreme price environment, Longi persists in maintaining high production levels, absorbing market share from mid to lower-tier manufacturers. This week witnessed some new major chemical manufacturers facing production halts and salary reductions due to sustained cash flow pressure, with a growing squeeze effect in the silicon material segment.

Demand Dynamics

Cash flow losses at the silicon wafer end remain in a stalled state, with deteriorating liquidity being the main trend across the entire segment. In the short term, silicon material demand support from wafer procurement continues to operate at an ice point level.

Trend Assessment

Major manufacturers exhibit strong price support intentions with minimal room for concessions. Mainstream n-type prices still remain stagnant around the 38 RMB/KG mark, but particular attention is needed as component-end volume pressure is gradually reverting back to the silicon material segment. If manufacturers continue to expand production capacity against the trend in Q3, leading to a rupture in marginal supply-demand balance, prices may incline towards a downward direction.

This week’s silicon wafer prices: The mainstream transaction price for P-type M10 silicon wafers is 1.20 yuan/piece; the mainstream transaction price for P-type G12 is 1.75 yuan/piece; the mainstream transaction price for N-type M10 is 1.10 yuan/piece; the mainstream transaction price for N-type G12 is 1.65 yuan/piece; the mainstream transaction price for N-type G12R is 1.45 yuan/piece.

Production and Inventory

In mid-month, the silicon wafer inventory level has not yet dropped below 4 billion pieces. From the distribution of silicon wafer inventory, the market share of leading manufacturers remains high. Although there are rumors of increase from 183N manufacturers, the market’s general acceptance is poor. In this transparent stage of inventory distribution, battery manufacturers clearly struggling with losses are finding it difficult to accept premium orders in the short term imbalance of supply and demand. Additionally, there is an excessive supply of 210R, facing pressure, and prices are showing some negative fluctuations in the central node.

Price Trend

In the short term, aside from some sizes experiencing short-term mismatches due to supply and demand rotation, causing price fluctuations, silicon prices remain in a low consolidation phase.

Battery Cell Prices

This week’s battery cell prices: Mainstream transaction price for M10 battery cells is 0.300 yuan/W, G12 battery cells at 0.320 yuan/W, mainstream transaction price for M10 monocrystalline TOPCon cells is 0.30 yuan/W, and for G12 monocrystalline TOPCon cells, it is 0.35 yuan/W.

Production and Inventory

Overall, battery production continues to be sluggish, with inventory levels around 1-1.5 months within the month.

Price Trends

The slowdown in component orders has limited the support for battery wafer prices. Battery manufacturers are currently adjusting production to maintain cash flow, with minimal losses being the best expectation for many professional manufacturers. The 210RN is being pressured due to oversupply of upstream silicon wafers, waiting for downstream 210R orders to increase to provide support.

Furthermore, the construction of battery wafer production capacity in the Middle East is steadily progressing. With downstream component capacity accelerating in the Middle East, the region’s battery wafer capacity may become a sought-after premium capacity. In the heterogeneous global photovoltaic industry chain, the premium attribute of overseas TOPCon cell production capacity with advanced technology is more evident.

Component Prices

This week’s component prices: 182 mono facial monocrystalline PERC components have a mainstream transaction price of 0.80 yuan/W, 210 mono facial monocrystalline PERC components have a mainstream transaction price of 0.82 yuan/W, 182 double-sided double-glass monocrystalline PERC components have a transaction price of 0.82 yuan/W, 210 double-sided double-glass monocrystalline PERC components have a mainstream transaction price of 0.84 yuan/W, 182 double-sided double-glass TOPCon components have a mainstream transaction price of 0.86 yuan/W, and 210 double-sided double-glass HJT components have a mainstream transaction price of 1.00 yuan/W.

Production and Inventory

In July, the component production continued to be sluggish, with output ranging around 44-46GW within the month, and there are fluctuation risks in inventory levels.

End-market Demand

① Overseas: In Europe, the summer vacation season is impacting transportation efforts significantly. According to the European pricing platform, a slight downturn in prices is observed due to a surplus in efficient component supply and demand. Some distributors are gradually reducing their inventory levels. It is crucial to note that the pre-pull effect of various countries’ tariffs is gradually weakening, adding more disruptive factors to the export of PV components in the second half of the year.

② Domestic: Currently, ground power stations continue with transportation efforts, while distributed systems are awaiting positive developments. This week’s prices remain stable, with ongoing negotiations in the actual transaction center. Major factories are stabilizing within the range of 0.78-0.80 yuan/W, with some offering at 0.76 yuan/W.