On August 22, InfoLink announced the latest prices in the photovoltaic industry chain.

Silicon Material Prices

The supply side of silicon materials has maintained a stable trend this period. It is expected that the overall new supply scale for August will align with previous estimates, reflecting a month-on-month decline. However, starting in mid-August, the reduction in crystal pulling activities by some leading companies is anticipated to have a certain impact on the market. If other specialized silicon wafer manufacturers also expect to reduce their crystal pulling activities in September, it will undoubtedly create a significant adverse effect on the demand side for silicon materials. Additionally, some silicon material companies are expected to conclude maintenance and increase their production and output in September, which may lead to a slight rebound in new supply from the bottom, potentially putting new upward pressure on already declining inventory levels on the supply side, further hindering the rebound momentum of silicon material spot prices.

Observing the purchasing order situation for silicon materials reveals a divergence. Some buyers have excess inventory of silicon materials that exceeds their actual usage and the overall level of crystal pulling remains low, leading to a lack of urgency in actual purchasing demand and a prevailing wait-and-see sentiment. Conversely, another group of buyers has gradually concluded their essential purchases for production, with the slight adjustments in mainstream market prices already completed. Given the generally pessimistic atmosphere regarding silicon wafer prices for September, buyers are indeed finding it difficult to bear a substantial increase in raw material prices.

In terms of inventory, the overall inventory levels on the supply side have significantly decreased. However, the distribution of backlogged inventory has changed; due to reduced production and concentrated shipments, the inventory levels of certain manufacturers have dropped to relatively optimistic levels.

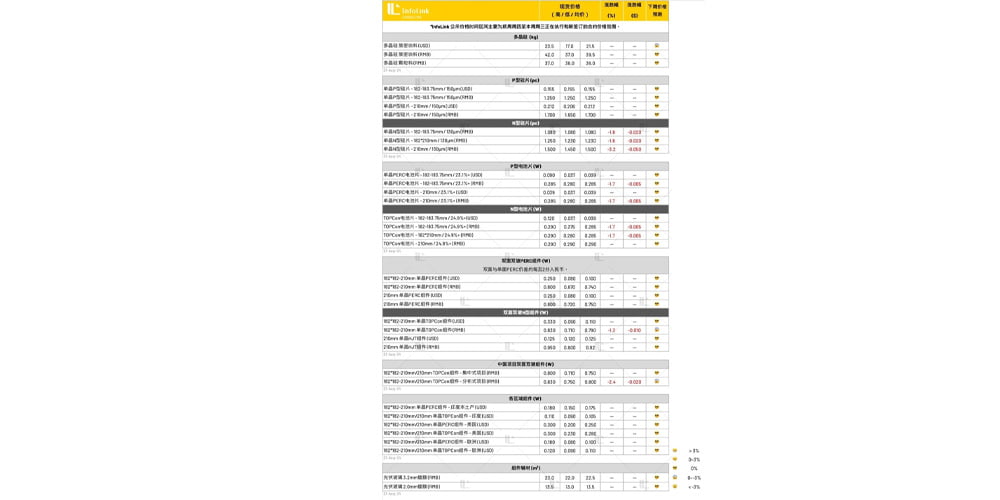

Silicon Wafer Prices

This week, silicon wafer prices have eased due to fluctuations in supply and demand, particularly with a slight decrease in N-type wafer prices. In the silicon wafer market, the dual pressures of rising silicon material costs and declining cell prices have made it challenging for wafers in the four segments.

Regarding prices, P-type wafer prices remained stable this week, with transaction prices for M10 and G12 specifications set at 1.25 RMB and 1.7 RMB per wafer, respectively. Conversely, prices for N-type wafers have loosened, with transaction prices for M10, G12, and G12R specifications at approximately 1.08 RMB, 1.5 RMB, and 1.23 RMB per wafer.

In terms of segmented markets, although specific transaction data has not yet been verified, there are rumors that the price for 183N type wafers has dipped to around 1.05-1.06 RMB per wafer. Meanwhile, some companies have quoted the price for 210N type wafers as low as 1.45 RMB per wafer, reflecting a decline of 6-7% compared to last week’s average transaction price. The 210RN specification faces downward pricing pressure as demand shifts toward the 183*210mm size, while current market inventory predominantly features 182*210mm sizes, resulting in relatively sufficient supply.

Looking ahead, despite recent market reports suggesting that leading companies might reduce production, any changes in actual operating rates are expected to start becoming apparent in September. The supply-demand relationship in August remains unstable, indicating a possibility of further downward trends in silicon wafer prices. Additionally, in overseas markets, it is observed that more top-tier manufacturers are adopting dual-distribution and contract manufacturing models in collaboration with battery manufacturers to maintain product competitiveness.

Battery Cell Prices

This week, the average transaction price of battery cells has decreased due to price adjustments made by leading companies. The prices for P-type M10 and G12 cells have dropped to between 0.28-0.285 RMB per watt. For N-type cells, the average price for M10 TOPCon cells also sits in the range of 0.28-0.285 RMB per watt. Meanwhile, the current prices for G12R and G12 TOPCon cells are maintained between 0.28-0.285 and 0.29 RMB per watt. Most companies report it is now challenging to uphold prices at or above 0.29 RMB per watt. As for HJT cell prices, they continue to remain in the range of 0.39-0.42 RMB per watt this week.

The recent trend in battery cell prices is primarily dictated by the extent of price reductions in module prices, with the battery cell segment lacking sufficient bargaining power. Only manufacturers capable of producing highly efficient cells can retain bargaining leverage above market levels. Moreover, the price range for lower-tier battery cells is still declining; for instance, lower-efficiency cells related to specific needs, such as those tied to inventory clearing, have seen prices drop to 0.27 RMB per watt or below

Component Prices

Currently, manufacturers are aggressively competing for orders, leading to a continued drop in execution prices. Some leading manufacturers are employing rather aggressive pricing strategies. Prices for concentrated projects have stabilized temporarily, with execution prices around 0.71-0.77 RMB per watt. Mid-tier and lower-tier manufacturers are still affected by order conditions, leading to lower discounted prices, with some recent execution prices approaching 0.7 RMB per watt. Project prices are influenced by manufacturers’ spot factory prices, which are still on a downward trend, hovering around 0.77-0.82 RMB this week. Overall, the average price for TOPCon has slightly adjusted to around 0.78-0.8 RMB, with a possibility of declining to 0.78 RMB by the end of the month.

The price range for 182 PERC double-glass modules is approximately 0.67-0.8 RMB per watt, with recent execution prices starting to fall below 0.7 RMB. HJT module prices range from 0.8-0.95 RMB per watt, with major project prices leaning towards the lower end, although manufacturers are maintaining prices close to 0.9 RMB.

Regarding BC, the price gap for P-IBC has stabilized at around 0.02 RMB compared to TOPCon, while the price gap for N-TBC currently remains between 0.05-0.07 RMB.

There are no clear signs of substantial recovery in demand yet. Demand support is expected to come from major domestic projects starting in August, while overseas demand remains steady. There are few buyers willing to accept rising quotes, leading to a market still filled with low-priced orders, inefficient products, and excess inventory, creating downward pressure on prices and disrupting market dynamics, making it difficult for component prices to recover.In the overseas market, HJT prices are around $0.12 to $0.125 per watt. PERC prices are approximately $0.09 to $0.10 per watt. There is significant price differentiation for TOPCon, with prices in the Asia-Pacific region hovering around $0.10 to $0.11. In the Japan and South Korea markets, prices remain at about $0.10 to $0.11 per watt. In Europe and Australia, prices are observed at €0.085 to €0.11 and $0.105 to $0.12, respectively. In Brazil, prices are about $0.085 to $0.11, while prices in the Middle East range from $0.10 to $0.11, with large project averages close to $0.10 per watt. Earlier orders have also been delivered at $0.15, and new contracts are signed at prices between $0.09 and $0.10, indicating considerable price variation. In Latin America, prices are around $0.09 to $0.11. The US market is influenced by policy fluctuations, leading to a decrease in project demand. Manufacturers are delivering new TOPCon modules at prices around $0.23 to $0.28, with previous contracts at about $0.28 to $0.30. The price difference between PERC and TOPCon modules is approximately $0.02 to $0.03. Going forward, InfoLink will adjust local manufacturing prices based on market conditions.