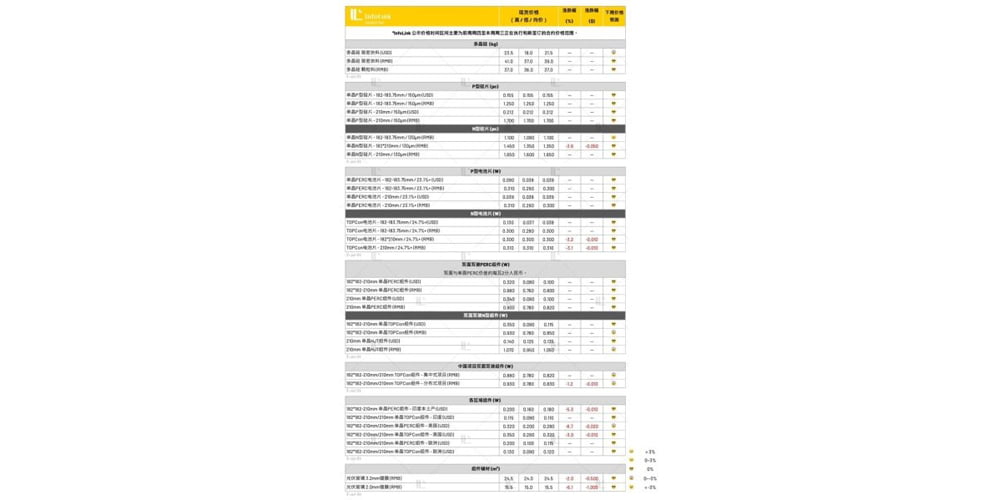

Silicon Material Price

The second half of the year has begun, marking the end of the downward trend in silicon material prices from the first half. Observing the market, overall prices remain stable, especially with major factory prices showing clear signs of stabilization and steadiness, ranging mainly from 38-41 yuan per kilogram. Prices for second and third-tier companies are maintained around 37-40 yuan per kilogram, with some second-tier companies also showing a relatively stable trend. However, companies with different characteristics are gradually reflecting different competitive strategies and marketing focuses, even being able to obtain a slight premium.Additionally, in terms of non-direct production materials, there is a high level of positivity shown towards the current price bottom, with increased inquiries and purchasing intentions, awaiting the response and impact after the launch of Chinese polysilicon futures at the end of the year. In terms of new supply this month, it is expected to continue the downward trend compared to the previous month, with more companies, including top enterprises, gradually increasing production cuts or maintenance scale, which is beneficial for stabilizing the current silicon material price bottom. In the short term, the inventory scale on the supply side may be contained, but it is still difficult to completely eliminate it for now.

Silicon Wafer Prices

Recently, there has been a gradual divergence in the price trend of silicon wafers based on specifications. The 183N silicon wafer saw a decrease in price due to previous low-cost clearance by companies and rapid depletion of inventory. At the same time, certain companies reported issues with silicon wafer quality due to material issues, leading to market tension signals. Some manufacturers have started negotiating price increases for this specification, with some quoting prices adjusting from 1.1 yuan per piece to 1.12 yuan per piece. However, as of this Wednesday, actual transactions have not been observed. As for the large-sized 210RN series, they remain relatively abundant with prices continuing to loosen and explore possibilities of shifting focus to small-size production.

This week, silicon wafer prices remain stable, with P-type silicon wafers in M10, G12 sizes transacting at 1.25 and 1.7 yuan per piece. N-type silicon wafer prices for M10, G12, G12R sizes transacted at around 1.08-1.1, 1.6-1.65, and 1.35 yuan per piece, respectively.Looking ahead, it is expected that the early July will be a crucial time point. Whether the experimental price increase for 183N by manufacturers will be implemented or not depends not only on the acceptance of battery manufacturers, but also on whether leading silicon wafer companies will follow suit, affecting the price trend of silicon wafers. The possibility of subsequent price increases will also be influenced by manufacturers switching production to 183N products. It is still unknown whether the mainstream transaction price for 183N will successfully rise next week.

Battery Cell Prices

Currently, the prices of battery cells in the large-size 210 N series (210RN/210N) are still on a downward trend, with sluggish end-demand also affecting the purchasing power of battery cells for the large-size 210RN/210N. This week, the prices of 210RN and 183N battery cells have officially reached parity per watt. Whether the competitive pricing of battery cells can stimulate the willingness of module manufacturers to advance their large-size product offerings remains to be seen depending on the specific projects.

In terms of other prices, P-type M10 and G12 sizes are maintained at 0.29-0.3 yuan per watt. As for N-type battery cells, the average price of M10 TOPCon battery cells also remains at 0.28-0.3 yuan per watt, with some even falling below 0.28 yuan per watt. The current prices of G12R and G12 TOPCon battery cells have dropped to between 0.3 and 0.31 yuan per watt. Meanwhile, HJT (G12) high-efficiency battery cells are priced between 0.45 and 0.55 yuan per watt.Looking ahead, as battery manufacturers continue to clear inventory at the end of the month, inventory levels remain stable. The rapid decline in prices of 210R and 210N batteries has led some production manufacturers to reduce production or even halt production on that line to alleviate losses. The production scheduling in July and the dynamics of end demand in the component sector are still the focus of attention among enterprises. Despite ongoing production surveys by InfoLink, a pessimistic atmosphere continues to persist in the market.

Component Prices

In early July, prices temporarily stabilized due to fewer overall project executions. This week, TOPCon component prices are roughly between 0.78-0.90 Chinese Yuan, with prices starting to trend towards 0.8-0.85 Chinese Yuan. Price competition at lower levels and rapidly decreasing prices for less efficient products can be observed, with prices as low as 0.74-0.78 Chinese Yuan per watt. Some manufacturers are even pricing their less efficient products at 0.78 Chinese Yuan. For other specifications, 182 PERC dual-glass module prices range from around 0.76-0.85 Chinese Yuan per watt, with a significant decrease in domestic projects leading prices gradually below 0.8 Chinese Yuan. HJT components have seen few recent project deliveries, maintaining a stable price range of around 0.93-1.07 Chinese Yuan per watt, inching closer to the 1-1.05 Chinese Yuan range and heading towards the 0.96-1 Chinese Yuan price range, where even large projects are priced below 1 Chinese Yuan.

However, observing the opening of tender projects, overall prices still show a downward trend. First-tier manufacturers have a significant price differentiation, with most still hoping to maintain prices at around 0.8 yuan in the third quarter, while some prices continue to drop to below 0.8 yuan per watt.

In the overseas market, prices have mostly stabilized this week, with TOPCon prices showing distinct regional variations. Prices in Europe and Australia still range between 0.09-0.125 euros and 0.11-0.13 US dollars, respectively. However, prices in Brazil and the Middle East are around 0.085-0.12 US dollars and 0.1-0.13 US dollars, with Latin America at 0.09-0.11 US dollars. PERC prices are around 0.09-0.10 US dollars per watt, while HJT prices are around 0.13-0.14 US dollars per watt.Looking ahead to July, component scheduling remains under considerable pressure, with the uncertainty of orders affecting scheduling possibly facing downward revisions, with a rough estimate placing domestic component production between 40-45 GW. The main reason continues to be the approaching summer vacation in Europe in July and August, resulting in a slowdown in shipments, with demand support only remaining in domestic and Middle Eastern markets, pending the execution of new projects.