Silicon Material

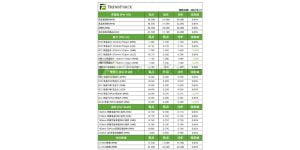

This week’s silicon material prices: The mainstream transaction price for monocrystalline re-purposed material is 34 RMB/KG, while the mainstream transaction price for monocrystalline dense material is 32 RMB/KG; the N-type material is quoted at 38 RMB/KG.

Trading situation: Monthly contracts have been largely completed, focusing on leading manufacturers; due to sustained losses at the downstream crystallization end, a “buy as needed” strategy remains in place, resulting in continued low trading volumes for silicon materials.

Inventory dynamics: As of this week, production cuts by major manufacturers and purchases by traders have slightly reduced the inventory levels of silicon materials. Current inventory levels are around 200,000 to 220,000 tons, and inventory pressure is expected to ease in the short term.

Price trend: This week’s prices remain stable, with a steady reduction in polysilicon supply, while demand is weak due to conflicting driving factors. Only some manufacturers with existing orders have shown restocking needs; however, ongoing losses and price declines continue to pressure the overall operating rate in the wafer segment. In the short term, silicon material prices are likely to maintain a sideways trend.

Silicon Wafers

This week’s silicon wafer prices: The mainstream transaction price for P-type M10 wafers is 1.15 yuan per piece; the mainstream price for P-type G12 wafers is 1.65 yuan per piece; the mainstream price for N-type M10 wafers is 1.08 yuan per piece; the mainstream price for N-type G12 wafers is 1.50 yuan per piece; and the mainstream price for N-type G12R wafers is 1.25 yuan per piece.

Supply and Demand Situation: On the supply side, current inventory depletion is challenging, making the adjustment of production strategies for leading specialized manufacturers critical at this stage. On the demand side, the battery segment is experiencing stagnation and restructuring, and overall procurement efforts are not optimistic. Integrated manufacturers have noticeably reduced their battery production, and the demand for external sourcing and outsourcing of silicon wafers is showing signs of fatigue.

Price Trends: Driven by high production from leading and specialized manufacturers, the supply redundancy of G10L has rebounded, with the mainstream transaction price decreasing to 1.08 yuan this week. Meanwhile, the overall inventory pressure on G12 (N and P types) has increased, putting some pressure on prices, with mainstream prices dropping to 1.50 yuan (N) and 1.65 yuan (P), respectively. Amid weakening demand in the battery sector, the dynamic adjustment of silicon wafer production will significantly impact price trends, with expectations that silicon wafer prices will continue to decline.

Battery Cells

This week, the prices of battery cells are as follows: the mainstream transaction price for M10 battery cells is 0.290 CNY/W, and for G12 battery cells, it is also 0.290 CNY/W. The mainstream transaction price for M10 monocrystalline TOPCon batteries is 0.275 CNY/W, while for G12 monocrystalline TOPCon batteries, it is 0.280 CNY/W.

Supply and demand situation: On the supply side, integrated manufacturers are changing their production scheduling strategies for battery cells. Some leading companies have begun to shut down certain battery cell production bases to prevent negative operating leverage from eroding their component profits. New entrants are also facing challenges, as many manufacturers, suffering losses, have had to reconsider their existing business profits, leading to either shutdowns or asset transfers. However, restructuring does not equate to the disappearance of existing production capacity. Additionally, the component sector has recently faced price pressures, with a strong willingness to transfer these pressures upstream.

Price trend: Amid the dual pressures of upstream price declines and downstream demand stress, the mainstream transaction centers for N-type M10 and G12R have shifted downward this week. The transaction price for N-type M10 has dropped below 0.28 CNY/W to 0.275 CNY/W, while N-type G12R has fallen below the 0.29 CNY/W threshold, adjusting down to 0.28 CNY/W. Looking ahead, the extent to which terminal demand in Q3 and Q4 can be realized will significantly impact battery cell prices.

Modules

This week’s module prices: The mainstream transaction price for 182 mm monocrystalline PERC modules is 0.71 yuan/W, while the price for 210 mm monocrystalline PERC modules is 0.73 yuan/W. The transaction price for 182 mm bifacial dual-glass monocrystalline PERC modules is 0.72 yuan/W, and for 210 mm bifacial dual-glass monocrystalline PERC modules, it is 0.74 yuan/W. The mainstream transaction price for 182 mm bifacial dual-glass TOPCon modules is 0.76 yuan/W, and for 210 mm bifacial dual-glass HJT modules, it stands at 0.90 yuan/W.

Supply and Demand Situation: It is expected that module demand in September and October may experience a slight month-on-month increase, with signs of improvement in order visibility. Additionally, module manufacturers are accelerating their overseas production capacity layout, particularly in the Middle East and Indonesia, to mitigate the impact of tariffs from certain countries.

Price Trend: Module prices have remained stable this week, but there continues to be a pressure for competitive pricing in future transactions.