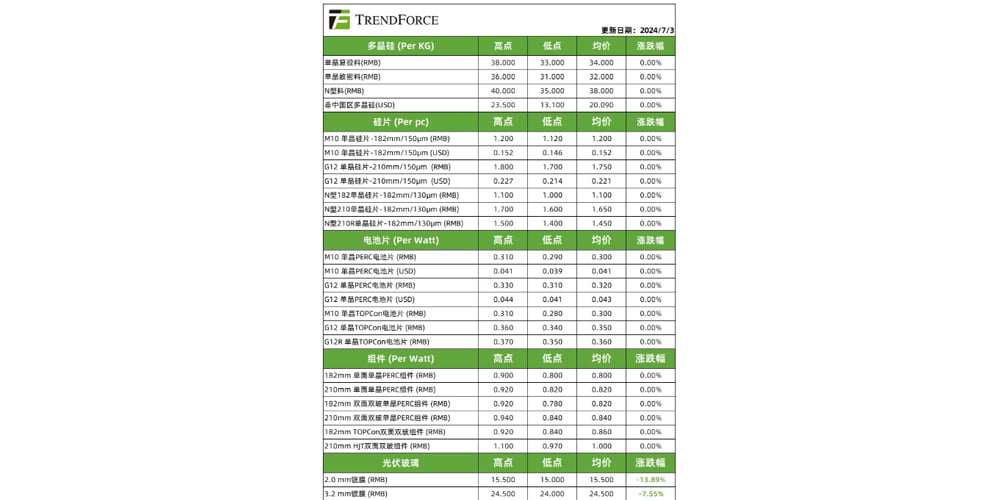

01 Silicon Material

Production Scheduling andThis week’s silicon material prices: The mainstream transaction price for single crystal recycled material is 34 yuan/KG, and the mainstream transaction price for single crystal dense material is 32 yuan/KG; N-type material is quoted at 38 yuan/KG. Trading Situation: This week, the overall silicon material signing situation has improved, with the volume of n and p-type silicon materials seeing a slight increase, but the signing mode still remains on a just-in-time procurement basis. Silicon material production schedule continues to remain sluggish. Production Situation: The new production capacity of the top two major factories in Q2 has basically reached full capacity, but the reduction caused by maintenance and shutdowns effectively offsets the increase in capacity, with overall silicon material production expected to reach around 150,000 tons in July. Production scheduling: Silicon material segment is temporarily stable. Inventory Dynamics: Inventory saw a slight increase at the end of June, considering the supply-demand gap in July as material enterprises ramp up production at the crystal pulling end, silicon material inventory is expected to continue to rise by the end of the month, but there is a shift in inventory from material enterprises gradually moving to the crystal pulling end. Trend assessment: This week, the price of silicon materials remains stable, with n-type offering at 38 yuan/kg, while second-tier manufacturers offer slightly lower prices. The overall market price remains steady, and price fluctuations may occur at the end of the month. It is necessary to observe the game situation between material suppliers and crystal pulling end to determine specific adjustments based on the digestion process of their own inventory in these two links.

02 Silicon Wafers

This week’s silicon wafer prices: The mainstream transaction price for P-type M10 silicon wafers is 1.20 yuan/piece; the mainstream transaction price for P-type G12 is 1.75 yuan/piece; the mainstream transaction price for N-type M10 silicon wafers is 1.10 yuan/piece; the mainstream transaction price for N-type G12 is 1.65 yuan/piece; the mainstream transaction price for N-type G12R silicon wafers is 1.45 yuan/piece. Production and Inventory Schedule:Production scheduling continues to shrink.The operating rate of silicon wafer segment in July was obviously differentiated. Leading and top-tier specialized manufacturers maintained high capacity utilization rates, leveraging cost advantages to capture market share from competitors. Integrated manufacturers, experiencing cost-price inversion, increased external procurement ratios. Meanwhile, mid-to-tail specialized manufacturers continued to uphold low operating rates, minimizing losses. It is anticipated that overall silicon wafer production in July will remain sluggish, ranging around 50-52GW, with end-of-month inventory levels expected to decrease to 30-40 billion pieces. Price Trend: The pressure of silicon wafer inventory is gradually easing.Silicon wafer prices rebound sentiment is growing, Despite the unsuccessful price increase attempts by some specialized manufacturers of N-type wafers, the trend of price hikes due to supply and demand constraints remains unchanged for certain sizes of N-type silicon wafers. The success of this trend depends on the extent of inventory digestion by the end of the month. There are ongoing orders for P-type silicon wafers in Q3. With limited existing production capacity for P-type wafers, some manufacturers are expecting price increases.

03 Solar Panels

This week’s prices for solar panels: The mainstream transaction price for M10 solar panels is 0.300 yuan/W, while for G12 solar panels it is 0.320 yuan/W. The mainstream transaction price for M10 monocrystalline TOPCon solar panels is 0.30 yuan/W, and for G12 monocrystalline TOPCon solar panels it is 0.35yuan/W. Production Inventory: The overall production trend of batteries remains sluggish, with some P-type capacity undergoing upgrade transformation, leading to a decrease in P-type output, while the overall output proportion of N-type has increased. The total battery cell production for the month is expected to fall within the range of 53-55GW. The production situation of secondary specialized manufacturers is not optimistic, with a decreasing trend in capacity utilization due to factors such as increased production by integrated manufacturers and reduced outsourcing. There is a risk of cash flow lagging behind or potential production shutdowns, and inventory pressure is expected to increase in July. Price Trends: Poor visibility of downstream component orders, insufficient demand support for battery cells overall, and varying supply-demand conditions for different sizes and types of battery cells. Increased production by some manufacturers has exacerbated a loose supply-demand situation, potentially leading to further price adjustment pressure for models like 210RN; if reduction in production for remaining models goes smoothly and stabilizes supply-demand conditions, a steady state may be able to maintain stability. 04 Components

This week’s component prices: the mainstream transaction prices of 182 mono-facial monocrystalline PERC modules is 0.80 yuan/W, 210 mono-facial monocrystalline PERC module is 0.82 yuan/W, 182 bifacial monocrystalline PERC module is 0.82 yuan/W, 210 bifacial monocrystalline PERC module is 0.84 yuan/W, 182 bifacial TOPCon module is 0.86 yuan/W, and 210 bifacial HJT module is 1.00 yuan/W. Production Inventory: The component production in July continues to show a weak trend, with output in the range of 44-46GW for the month and a noticeable upward trend in inventory levels. End demand: ① Overseas: Changes in the tariff policy for PV modules in South Africa have led to a flood of low-priced modules entering the overseas market. As a result, countries are taking a cautious approach to their PV module import policies, with a growing demand for localization of PV manufacturing; ② Domestic: Installation continues to progress, but there is a lack of momentum in distributed energy. Price Outlook: Actual transaction prices continue to be under pressure, with a sustained downward trend in transaction centers. In July, top manufacturers are generally facing insufficient orders, entering a period of demand vacuum. Some manufacturers are competing aggressively to survive, leading to further reductions in shipment prices.

05 Photovoltaic Glass

This week, the price of photovoltaic glass has decreased: The transaction price of 2.0mm coated photovoltaic glass is 15.5 yuan/sqm, and the transaction price of 3.2mm coated photovoltaic glass is 24.5 yuan/sqm. Price Trend: The price of photovoltaic glass has decreased this week, with a 13.89% decrease in the price of 2.0mm coated photovoltaic glass to 15.5 yuan/sqm, and a 7.55% decrease in the price of 3.2mm coated photovoltaic glass to 24.5 yuan/sqm. Supply and Demand Situation: ① On the supply side, currently, the operational capacity of domestic photovoltaic glass is 115,340 tons/day, with production capacity continuing to increase, leading to an overall increase in supply. ② On the demand side, visibility of downstream component orders has decreased, resulting in a decline in demand for photovoltaic glass; it is expected that in July, the imbalance between supply and demand for photovoltaic glass will worsen, putting further pressure on prices. Production Scheduling: Looking ahead to July objectively, the production of photovoltaic glass is still under pressure, with the uncertainty of orders affecting production, potentially leading to a downward revision in overall photovoltaic glass production, continuing the trend of sluggishness.